The government and business media and sideline observers want to call your business small. That categorization applies to more than 99% of business firms in the USA. So someone’s missing something about the nature of the business economy. Small business makes the biggest contribution.

The error lies in misunderstanding systems thinking. The reason why people start and nurture small businesses is that they have an imagined idea for a new and better future – a better product, a better service, a better membership club, a better environment for office workers, whatever it may be – and they work with other people to try to bring it about. The other people they work with may be customers, partners, supply chain elements or employees; the business owner figures out the best network. The network and the connections and the information flows are never small. Today, thanks to the internet and collaboration software and communications, the network is the whole world. Any so-called small business can link to and orchestrate the world’s resources, the world’s designers, and the world’s imagination to bring value to its customers. What’s small about that?

Cynthia Kaye is one small business owner and consultant who fully recognizes the implications of thinking about the scale of the network rather than the scale of one node. First, it requires big thinking. What is the best way to harness the global resources to which business has access? What is the best service for customers? What’s the best way to provide service to customers?

For example, in her own business of video production, she has defined many ways in which her company can be the best. For example, being the best at getting the most out of the client’s budget. That’s a compelling value proposition and a genuinely unique claim. To deliver requires knowledge, experience, imagination, creativity, relationships, control, and meticulous attention to detail – all of which can be combined in an unsurpassed combination recognized by clients as superior.

Economic growth and value creation come from using imagination and experience to create new knowledge: a surprise, a revelation, an exceeding of expectations. Imagination is not a product of scale but of creativity.

Cynthia translates this big thinking into big opportunity. Often, this comes from growing with a client. That growth can begin parallel with a small customer – growing together through co-creation and collaboration. It can also come from small business supplier serving big business so well that more and more revenue is directed their way. The resultant shared growth benefits both parties. Is that big or small? It’s actually unrestrained, unlimited, unbounded.

From this collaborative networked co-creation process comes big success. We know from Hermann Simon’s database of Hidden Champions that so-called small business can outperform big business in many ways, including higher revenue per employee, higher profit margins, greater employee retention, longer and stronger customer relationships, and more innovation and investment in R&D and new projects and capital equipment. Hidden Champions is a better descriptive term than small business.

Small business shouldn’t be hidden or ignored – it should be celebrated, lauded, cheered on and loved. Small business is the economic system that generates the prosperity we all enjoy.

The Wall Street Journal (June 26, 2023) reported on its front page that “small companies have been responsible for all of the net job growth in the US since the onset of the Covid-19 pandemic and account for nearly 4 of 5 available job openings”. They’ve hired a net 3.67 million people, while larger establishments have cut a net 800,000 jobs during that same time period. “Small businesses are literally holding up the job market”, said Aneta Markowska, chief economist at Jefferies, who compiled the data.

Disregarding the size-shaming of referring to these powerhouse growth-producing businesses as “small”, this should be all good news, shouldn’t it? Well, not in the eyes of the Wall Street Journal. The surge of hiring by these businesses “can be bad news for markets” (by which they mean the casino stock trading markets of Wall Street). All this hiring is driving inflation, and may complicate the Federal Reserve’s efforts to cool that inflation, according to WSJ. The Fed wants to “slow down the labor market and weaken the economy” and small business job creation gets in their way. But don’t worry, say the WSJ reporters, “The Fed has said it plans to continue to increase rates this year ….to slow the economy” and hit these pesky small businesses with a downturn that will reverse their annoying optimism.

This is all typical of the financial establishment. The growth of the financial sector in the economy comes at the expense of the productive sector. A recent Bank of International Settlements (BIS) analysis shows a negative relationship between the rate of growth of the financial sector and the rate of growth of total factor productivity. The so-called small businesses highlighted in the WSJ report are, in spite of the expanding financial sector, bringing economic growth to the nation, and creating jobs for breadwinners and their families, reducing welfare dependence. They are producing new value, which is what entrepreneurs do, and generating new sales and revenues by pleasing customers. The financial establishment can’t stand it!

The growth of the financial sector, focused on stock trading and bond trading related to the few thousand companies in the quoted market indexes is detrimental to the productive economy and the 6+ million employer businesses that comprise it. The trading has nothing to do with financing productive investment in innovation. Once a company has completed an IPO, it generally never goes back to the stock market for equity financing. For example, the only money that Apple has ever raised from the public stock market in its history is the $97 million realized from its IPO in 1980. All of the stock splits and stock buybacks since then have been for the benefit of stock traders (don’t call them investors – they’re not) and incumbent management who grant themselves stock awards and stock options. There are accounting years when Apple has often spent a sum greater than its net income on stock buybacks. In other words, it is diverting resources away from productive investment and into stock market manipulation.

While “small” entrepreneurial businesses are innovating, creating new value and new jobs, the big corporations entangled in the financial sector are destroying jobs and extracting value through their manipulation of stock markets and stock prices. The Wall Street Journal reports admiringly.

https://hunterhastings.com/wp-content/uploads/2023/01/shutterstock_1210529431-scaled-e1674776742737.jpg5502560Hunter Hastingshttps://hunterhastings.com/wp-content/uploads/2021/03/hh-logo-blk.svgHunter Hastings2023-01-26 15:48:392023-01-26 15:48:40WSJ Has No Respect For Entrepreneurial Businesses, Even When Reporting Their Success.

There are roughly 32 million businesses in the US, of which 99.9% are what the government calls “small”. This classification of business accounts for about half of GDP and of total employment (making it just as productive as “big business”), and usually more than half of new job creation (making it more dynamic than big business). It’s often where innovation first enters the market, since small business is more open to risk taking than big business. If we remove the Fortune 500 and the Russell 5000, we’ve still got 32 million, rounded up, so let’s think of them as a community.

Within the 32 million, there is a wide range of size, whether measured by revenue or number of employees. The government in the form of the SBA (Small Business Administration) uses a range of up to 500 employees and a revenue of $7 million per year. But they also relax this range in different classification categories; their “small” financial and insurance business range goes up to 1,500 employees and $38.5 million in revenues. Clearly, there’s no consistency or integrity in their definitions, and not much useful information.

A better way to look at these businesses is as an integrated network of productivity, information flow, knowledge-building, innovation and value creation.

Productivity:

Dr. Samuel Gregg in his book The Next American Economy identifies the decline in the formation of new entrepreneurial businesses as responsible for the significant decline in American productivity. These businesses have an intensified motivation to be productive; it’s hard to get capital, so they need to make the most of what they’ve got and find agile ways to borrow, rent or originate capital. They can’t afford productivity-sapping bureaucracy. They find ways to accelerate cash flows. They adopt new technological innovations quickly so as to take advantage of productivity enhancements. Productivity is essential for them.

Knowledge-building:

Bartley J. Madden in his book Value Creation Principles, identifies knowledge-building proficiency as the fundamental driver of firm performance. In the integrated 32-million strong network of businesses we are analyzing, information flows faster and more freely as a result of more network nodes, more connections between nodes, and lack of barriers to learning such as bureaucracy. These businesses know they must learn at speed, apply their learning fast and use it to serve customers better. There’s no learning time to lose.

Dynamic Efficiency:

Efficiency is an economic concept that hasn’t been very helpful for business in general. It tends to mean doing less with less: cutting costs, saving on inputs, not risking innovation, not attempting experiments with uncertain outcomes. But economist Jesus Huerta de Soto developed the contrasting concept of dynamic efficiency: fast adaptation to changing customer preferences, and rapid creation and adoption of new market knowledge, with an economy of time and agile decision-making. This is the entrepreneurial method, and the way that the 32 million competes effectively with larger, better resourced but less agile firms.

Pure value creation:

Businesses generate cash flow as a result of the valuable customer experiences they enable. The value that customers perceive turns into willingness to pay, resulting in cash flow that is the life blood of small businesses who have less access to credit and debt to fund their working capital needs. The 32 million are acutely sensitive to cash flow, and therefore to customer value. They remove all obstacles to customer value, including bureaucracy, complicated service arrangements that obscure value visibility and take time, and any other obstructions they can identify. These businesses know that they must pursue pure value creation.

Customer focus:

The disciplines of dynamic efficiency and pure value creation demand an intense customer focus. The 32 million choose their customers carefully, develop a deep knowledge of them and their needs, nurture empathy to get on the same wavelength with customers regarding those needs, and are constantly listening for feedback and adjusting to any new signals that come through the feedback channel. This intensity of customer focus sustains the innovation and elevated quality of service that, in turn, secures continuity and strengthening of business relationships. That’s why these businesses are the backbone of the economy.

Unentangled with government:

The greatest barrier to all business-driven economic growth, progress and innovation is government. Both taxation and regulation are business-killers by intent. Big business becomes entangled with government. They develop big bureaucracies to comply with regulation, keeping them close to government and saddling the 32 million with disproportionate compliance costs if they’re forced to match big-business compliance practices. And big businesses assemble lobbying forces and budgets to design, write and pay for government approval for regulations that protect them and over-burden others. It’s this entanglement with government that condemns big business to permanent inefficiency, and also results in the kind of government-directed surveillance scandals that are currently being uncovered.

The 32 million is in no way small. It’s the vital, leading edge group that brings innovation, growth, development and dynamism to the economy. Let’s find another term than “small business”.

https://hunterhastings.com/wp-content/uploads/2021/04/shutterstock_1246843396-scaled-e1618348656679.jpg12162534Hunter Hastingshttps://hunterhastings.com/wp-content/uploads/2021/03/hh-logo-blk.svgHunter Hastings2023-01-04 09:26:132023-01-04 09:26:14No businesses are “small”. They’re all productive nodes in a tightly connected knowledge-building value-creating network.

There’s a middle class of businesses that are the backbone of the economy. Professor Saras Sarasvathy coined that term, and we’re pleased to adopt it.

These businesses sit between the big corporations of the major stock indexes and the VC-funded gazelles and unicorns of Silicon Valley and Silicon Hills. The watchwords for these backbone businesses are duration and durability. They last and prosper because they are well-run, following the entrepreneurial method.

Entrepreneurship is usually portrayed from the perspective of ends: identifying unmet customer needs, creating new and innovative solutions, taking them to market, making a success.

That’s all true. However, there is another perspective that comes from actually running a business, ensuring that operations are smooth and efficient, monitoring daily cash flows and monthly P&Ls, and managing people’s performance.

Often, running a business requires an intensified focus on means. Cash flow, operations, employee performance — these are means, and running a business is a science of managing means. Business advisor Andrew Frazier helped us focus on means in this week’s Economics For Business podcast.

Key Takeaways & Actionable Insights

Knowledge is an entrepreneurs most important means. Accumulate it purposefully (but not by losing money).

The more you know, the more you grow. That’s a mantra from Andrew Frazier. He advises thoughtful accumulation of knowledge. One way to learn is to lose money — you learn what doesn’t work, and what not to do. Avoid this form of learning by purposive knowledge gathering. This includes truly knowing your purpose — at least part of which is to build the business resiliency that delivers durability and duration.

Knowing your numbers is a critical component of durability and duration, and of shepherding your means.

In his advisory and consulting roles, Andrew encounters many business owners who don’t know their own numbers intimately — their daily cash inflows and outflows, the precise identification of fixed and variable expenses, the condition of the P&L and the balance sheet. Some, he says, fear the numbers. They delegate accounting to an outside service, or even to an internal “back room” employee. Don’t delegate “knowing your numbers” to anyone. Be on top of them every day. They tell you your means.

Sales and marketing are the most important means of lasting business growth, and not necessarily expensive.

There is no business without the sales and marketing activities that identify the right customer niche and tell your story to those customers in a credible, warm and persuasive fashion. Many business owners and entrepreneurs see sales and marketing as an expense to be incurred only if there is cash leftover from other variable and fixed costs that take precedence. This is wrong-way thinking. Sales and marketing are job #1.

Hiring employees is the biggest change you will make to your business and to your role in it.

You want to hire employees for the growth of your business. As you do so, you are changing your business. You change its structure: it now needs organizational design. You change your role: you are now a leader. You change the business’s operational flow because it now needs detailed processes and systems. You change the culture: it becomes more indeterminate and therefore requires more of your attention. You stop working in your business and start working on it.

Duration and durability require sacrifices from you.

One aspect of the entrepreneurial ethic is personal sacrifice today for market reward in the future. Sacrifice is part of your means. You’ll work harder and longer hours. Your business and social and family lives will become inextricably intertwined. Your business will become your identity. Realize this and embrace it.

A lasting business requires an exit plan.

A business that prospers over an extended period needs an exit plan for its owner or founding entrepreneur. This can range from an IPO or sale to an acquirer to leaving it to your kids or turning it over to employees. Whatever the case, the owner needs to plan ahead for exit, almost from the beginning. For example, if you have a professional services business, what will make it saleable when you want to exit? Is there asset value over and above revenue flow? Will customers stay after you leave? Are your kids even interested?

https://hunterhastings.com/wp-content/uploads/2021/06/e4b-cover-122.jpg5321250Hunter Hastingshttps://hunterhastings.com/wp-content/uploads/2021/03/hh-logo-blk.svgHunter Hastings2021-06-16 04:39:442021-10-11 10:38:35122. Andrew Frazier on Running Your Business

[postintro]There are many reasons to elevate entrepreneurship as the institutionally-approved and institutionally-accelerated pathway to economic success for everyone. Community flourishing through self-help is one of them. I’m supporting the team behind Entrepreneur Zones, focused efforts for enhanced performance of small businesses in targeted locations in economically under-performing geographies [/postintro]

2020 witnessed small businesses across the country struggling to adapt and survive during the government-imposed pandemic lockdowns. And while some were able to pivot their services and business model to serve an increasingly digital market, many were forced to shut down for good, leaving thousands jobless.

The closure of these businesses is one of this year’s biggest tragedies. The economic impact of these closures will continue to be felt for many years to come. If we have collectively learned anything this year, it’s that America relies on small business entrepreneurship to flourish and prosper.

Entrepreneurship is empowerment

Nowhere is the empowering potential of small business entrepreneurship more prominent than in our small-town Main Streets and local communities. Even through the pandemic, we’ve seen small businesses all across the country step up and change the way they operate in order to help their communities. Via a quick search around the internet, you can find dozens of examples of small businesses doing their part: from local pharmacies doing Covid testing to distilleries manufacturing hand sanitizer and restaurants providing free meals.

These entrepreneurs and workers were faced with an existential crisis like they’ve never seen before. Their response? Do good for the community. There’s something about small businesses that is just so inspiring.

Ultimately, entrepreneurship is the backbone of these communities, and provides both residents and the local economy the opportunity to grow as these businesses grow. What’s more, entrepreneurship is not just for the rich, it is for everyone. Building a business from the ground up is no small feat, but it is something that’s achievable by anyone, regardless of background. Through entrepreneurship, people can pull themselves up and bring new economic value to their communities and to themselves.

The potential of Entrepreneur Zones

Heading into 2021, we need to place a renewed focus on encouraging entrepreneurship in our small towns and cities. The key to this could be Entrepreneur Zones – targeted areas within economically-distressed communities where new entrepreneurship-focused initiatives can help local business get their start, and help those that have already started to thrive. Policy initiatives can include relaxed regulations, tax incentives to encourage investors, focused education and training, and the kinds of mentoring and interconnection that help businesses integrate into larger value-creation ecosystems.

Dale G. Caldwell of Fairleigh Dickinson University’s Rothman Institute of Innovation and Entrepreneurship notes, “To accelerate small business employment, government could provide entrepreneur grants and issue small business bonds through the Small Business Administration specifically for the businesses in federally approved entrepreneur zones. These programs would not be a burden on taxpayers and potentially lead to an injection of billions of dollars into businesses…that desperately need a lifeline to survive.”

As more than 11 million people look for new opportunities, these small businesses could help provide the jobs needed to both keep food on the table for struggling families and spur economic growth at the national level.

Further, many in the growing pool of unemployed Americans are skilled workers who have been through the training and education for their jobs. The talent is there, what is needed is the capital to invest in these businesses.

The future lies in small businesses

We’re dealing with a once-in-a-lifetime crisis, and we need to work to establish apolitical policies that support our nation’s small businesses. Nearly 50% of America’s GDP output and nearly 50% of all American workers are employed by small businesses. It’s time that we began to recognize and reciprocate the values and utility that small businesses provide to this country.

And it’s not just local, it’s global. For example, Scott Livengood of Arizona State University is part of a team offering Education For Humanity – a program of education, and entrepreneurial skill training for conflict-displaced refugees in countries like Uganda and Lebanon. Entrepreneurship provides a pathway out of not only America’s distressed inner cities, but out of distressed environments of all kinds, all over the world. Over the past half-century, we’ve seen that entrepreneurial and educational expansion into underdeveloped regions and markets is one of the best ways to raise people out of poverty and equip them with the skills and resources they need to prosper.

Across the world, we see just how important creating avenues for entrepreneurship is to keeping economics vibrant and resilient. In 2021, one of our top economic priorities should be to create more of these avenues.

https://hunterhastings.com/wp-content/uploads/2021/02/shutterstock_634282571-scaled.jpg19492560Hunter Hastingshttps://hunterhastings.com/wp-content/uploads/2021/03/hh-logo-blk.svgHunter Hastings2021-02-08 09:29:252021-02-08 09:29:25Empowerment Through Entrepreneurship.

Recently, on the Human Action Podcast, Jeff Deist and I discussed the Rothbardian theory of the entrepreneurial economy in chapter 8 of Man, Economy, and State, titled “Production, Entrepreneurship, and Change.” In this article I will illustrate just how this Austrian theory is applied effectively in the business world.

In chapter 8, Rothbard establishes the principles of what he calls the progressing economy, one in which gross investment in capital goods is increasing, productivity is growing, and firms are making profits, indicating social affirmation that they are deploying resources in the ways best adjusted to the most urgent and evolving consumer needs. Specifically, firms are making an economic profit—returns higher than the going rate of interest derived from social time preference.

Importantly, economic profits (returns higher than the cost of capital) are hard to achieve and even harder to maintain. Rothbard points out that, to succeed in this challenge, entrepreneurs must demonstrate superior foresight and judgment, and practice continuous dynamic improvement in their assembly and reassembly of assets to serve the consumer. This urgency is sharpened by the competition of new entrepreneurs who see the high returns that the pioneering entrepreneur has achieved and are willing to enter the same space for lower margins so long as returns remain higher than the going interest rate. Eventually, all the superior returns will be competed away—unless the first entrepreneur keeps changing and advancing to serve more and higher-valued consumer needs.

More specifically, Rothbard’s construct is that economic profit is the result of entrepreneurs identifying discrepancies in the capital structure where capital is overdeployed in the service of less acutely felt consumer wants and underdeployed in the service of some more acutely felt consumer wants. The function of entrepreneurship is to make the adjustment that consumers are demanding. Entrepreneurs buy factors that are underpriced because of the discrepancy and recombine them to serve currently underserved needs. The adjustments are always in the direction of higher and higher productivity. The prices of the new consumer goods and services generate a profit and a return that is higher in the new, adjusted arrangement of factors than in the prior arrangements.

Rothbard also deduces that the economic profit margin will erode over time because more entrepreneurs, seeing the high return for the new arrangement, will enter the economic space and compete away the high returns, pulling them down toward the going interest rate. Entrepreneurs must continue to find more new urgent consumer needs to address, rearrange their capital structure even further, and maintain a continuous dynamism both in their capital structure and in their consumer offerings.

Man, Economy, and State is a treatise of Austrian economic theory. To what extent is it translatable to and applicable to the realities of business in 2020? The answer is that Rothbard’s acute theoretical insights can be applied directly in business strategy to great effect.

A recent McKinsey Insights article confirms every one of Rothbard’s theoretical points in real-world analysis.

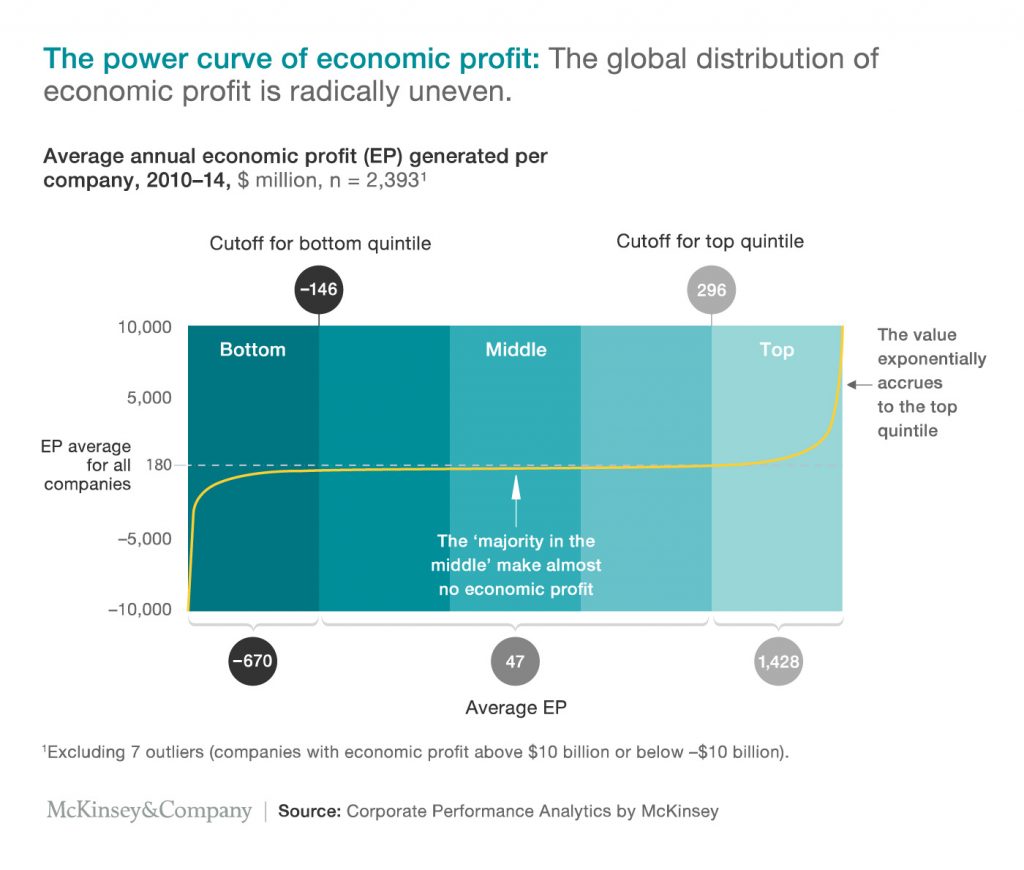

First, the McKinsey consultants confirm the challenges inherent in the effort to achieve economic profit. Their S-curve distribution (they call it a “power curve” for marketing purposes) illustrates how very few firms make high economic returns and most hover close to, or in some cases below, the break-even (i.e., zero economic profit) line.

The McKinsey consultants conclude that:

Market forces are pretty efficient. The average company in our sample generates returns that exceed the cost of capital by almost two percentage points, but the market is chipping away at those profits. That brutal competition is why you struggle just to stay in place. For companies in the middle of the power curve, the market takes a heavy toll. Companies in those three quintiles delivered economic profits averaging just $47 million a year.

The curve is extremely steep at the bookends. Companies in the top quintile capture nearly 90 percent of the economic profit created, averaging $1.4 billion annually. In fact, those in the top quintile average some 30 times as much economic profit as those in the middle three quintiles, while the bottom 20 percent suffer deep economic losses. That unevenness exists within the top quintile, too. The top 2 percent together earn about as much as the next 8 percent combined. At the other end of the curve, the undersea canyon of negative economic profit is deep—though not quite as deep as the mountain is high.

With further data analysis, the McKinsey consultants identify the strategic actions that need to be taken to place a firm in the highest echelons of economic returns in their industry—and they confirm all the implications of Rothbardian theory. They propose five strategies of adjustment that effectively derive directly from Austrian theory.

First, they confirm the importance of continuous dynamic reallocation of resources by firms in order to achieve high returns.

Winning companies reallocate capital expenditures at a healthy clip, feeding the units that could produce a major move up the power curve while starving those unlikely to surge. The threshold here is reallocating at least 50 percent of capital expenditure among business units over a decade. When Frans van Houten became Philips’ CEO in 2011, the company began divesting itself of legacy assets, including its TV and audio businesses. After this portfolio restructuring, Philips succeeded at reinvigorating its growth engine by reallocating resources to more promising businesses (oral care and healthcare were two priorities) and geographies. Philips started, for example, managing performance and resource allocations at the level of more than 340 business-market combinations, such as power toothbrushes in China and respiratory care in Germany. That led to an acceleration of growth, with the consumer business moving from the company’s worst-performing segment to its best-performing one within five years.

They also identify an accompanying strategy for dynamic allocation of resources in the form of frequent M&A (mergers and acquisitions) activity—buying new assets and selling old ones. They call this strategy programmatic M&A: continuously buying and selling capital assets and turning over factors to dynamically manage capabilities.

You need a steady stream of deals every year, each amounting to no more than 30 percent of your market cap but adding over ten years to at least 30 percent of your market cap. Corning, which over the course of a decade moved from the bottom to the top quintile of the power curve, shows the value of disciplined M&A. Corning understands that doing three deals a year means it must maintain a steady pipeline of potential targets, conduct due diligence on 20 companies, and submit about five bids.

Beyond reallocation and M&A, strong capital expenditure is required to maintain profits.

You meet the bar on this lever (strong capital expenditures) if you are among the top 20 percent in your industry in your ratio of capital spending to sales. That typically means spending 1.7 times the industry median. Taiwanese semiconductor manufacturer Taiwan Semiconductor Manufacturing Company (TSMC) pulled this lever when the Internet bubble burst and demand for semiconductors dropped sharply. The company bought mission-critical equipment at the trough and was ready to meet the demand as soon as it came back. TSMC had been in a head-to-head race before the downturn but pulled clear of the competition after it ended because of its investment strategy. That laid the foundation for TSMC to become one of the largest and most successful semiconductor manufacturing pure plays in the world.

In addition, it is critical to maintain a strong productivity program.

This means improving productivity at a rate sufficient to put you at least in the top 30 percent of your industry. Global toy and entertainment company Hasbro successfully achieved the top quintile of the power curve with a big move in productivity. Following a series of performance shortfalls, Hasbro consolidated business units and locations, invested in automated processing and customer self-service, reduced head count, and exited loss-making business units. The company’s selling, general, and administrative expenses as a proportion of sales fell from an average of 42 percent to 29 percent within ten years. Sales productivity lifted, too—by a lot. Over the decade, Hasbro shed more than a quarter of its workforce yet still grew revenue by 33 percent.

The fifth strategic lever is improvements in differentiation. Modern Austrian economics identifies the importance of differentiation in Per Bylund’s islands of specialization theory and our focus on brand uniqueness as a source of superior profits. McKinsey uses gross margin as a proxy for differentiation, and their consultants say:

For business-model innovation and pricing advantages to raise your chances of moving up the power curve, your gross margin needs to reach the top 30 percent in your industry. German broadcaster ProSieben moved to the top quintile of the power curve by shifting its model for a new era of media. For example, it expanded its addressable client base by using a “media for equity” offering for customers whose business would significantly benefit from mass media but who couldn’t afford to pay with cash. Some of ProSieben’s innovations were costly, sometimes even cannibalizing existing businesses. But, believing the industry would move anyway, the company decided that experimenting with change was a matter of survival first and profitability second. ProSieben’s gross margin expanded from 16 percent to 53 percent during our research period.

Each one of these Rothbard-derived strategies can be effective in driving superior returns. Even more effective is to combine them, a recommendation with which Rothbard would concur.

Big moves are most effective when done in combination—and the worse your endowment or trends, the more moves you need to make. For companies in the middle quintiles, pulling one or two of the five levers more than doubles their odds of rising into the top quintile, from 8 percent to 17 percent. Three big moves boost these odds to 47 percent. To understand the cumulative power of big moves, consider the experience of Precision Castparts Corp. (PCC). In 2004, the manufacturer of complex metal components and products for the aerospace, power, and industrial markets was lumbering along. Its endowment was unimpressive, with revenues and debt levels in the middle of the pack, and the company had not invested heavily in R&D [research and development]. PCC’s geographic exposure was also limited, though the aerospace industry experienced enormous tailwinds over the following ten years, which helped a lot.

Most important, however, PCC made big moves that collectively shifted its odds of reaching the top quintile significantly. The company did so by surpassing the high-performance thresholds on four of the five levers. For mergers, acquisitions, and divestments, it combined a high value and large volume of deals between 2004 and 2014 through a deliberate and regular program of transactions in the aerospace and power markets.

PCC also reallocated 61 percent of its capital spending among its three major divisions, while managing the rare double feat of both productivity and margin improvements—the only aerospace and defense company in our sample to do so. While nearly doubling its labor productivity, PCC managed to reduce its overhead ratio by three percentage points. It lifted its gross profit-to-sales ratio from 27 to 35 percent.

The combination of a positive industry trend and successful execution of multiple moves makes PCC a showcase of a “high odds” strategy and perhaps explains why Berkshire Hathaway agreed in 2015 to buy PCC for $37.2 billion. Could our model have predicted this outcome? Based on the moves PCC made, its odds of rising to the top were 76 percent.

McKinsey’s reputation in business strategy consulting is second to none. To see these consultants apply Austrian economic theory so directly in their recommendations is a strong confirmation of its value.

https://hunterhastings.com/wp-content/uploads/2020/08/shutterstock_1028158363-scaled.jpg14312560Hunter Hastingshttps://hunterhastings.com/wp-content/uploads/2021/03/hh-logo-blk.svgHunter Hastings2020-08-06 09:02:012020-08-23 11:38:36How Murray Rothbard’s Theory of Entrepreneur-Driven Progress Can Be Applied to Modern Businesses